FHA Loans

Federal Housing Administration (FHA) loans are government loans that are great in many situations to assist borrowers with qualifying for a mortgage. In many cases it is the only option for a lot of borrowers, and therefore is an excellent path to homeownership. The Department of Housing and Urban Development (HUD) oversees and creates the guidelines for FHA loans.

While we are the actual lender on an FHA loan, in exchange for our following the rules of FHA, HUD will insure the loan for us. Meaning, if our borrower were to default on an FHA loan, HUD will assist with covering our loss. Because of this insurability, FHA loans for some borrowers may come with better loan terms and easier qualifying guidelines.

Why would you want an FHA loan?

1. FHA is great for borrowers with little amounts of cash. It is a 3.5% down payment minimum, and you can borrow all the way up to $1,249,125

2. FHA is great for borrowers with lower credit scores. You can borrow the most amount of money with higher debt-to-income-ratios allowed, with the lowest credit scores, with this loan. And you can always put down as little as 3.5% down.

3. FHA is great for borrowers with past credit difficulties too, including bankruptcies and foreclosures, because these loans have the shortest waiting periods. (2+ years bankruptcies, 4+ foreclosures)

Your credit score has a minimal impact on the interest rate on an FHA loan. It has no impact on the mortgage insurance costs. This is the opposite of how a conventional loan works. On a conventional loan, your credit score has a large impact on your interest rate and mortgage insurance costs. And so for applicants with lower credit scores and lower down payments, FHA financing may be the best option. For applicants with higher down payments and higher credit scores, conventional financing may provide better terms.

Why would you not want an FHA loan?

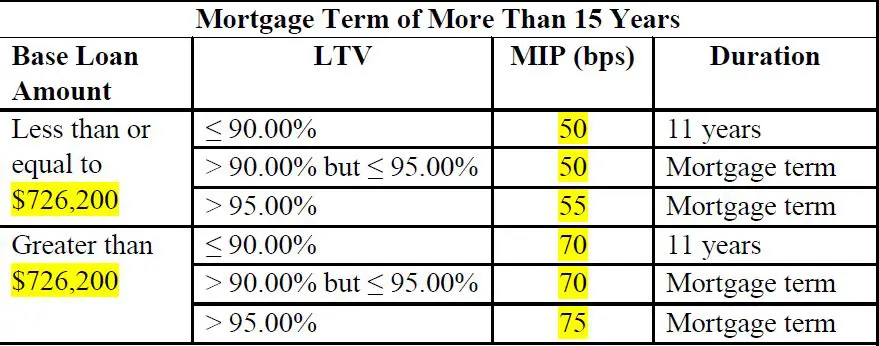

FHA loans typically have lower interest rates than conventional loans. However there are fewer loan options to choose from, you’ll typically find only a 5 year adjustable rate, a 15 year fixed rate, and a 30 year fixed rate. What unfortunately comes with a lower interest rate, is (sometimes) a higher mortgage insurance premium. Depending on the credit score and down payment, we’ll do the math and see which is lower. Here are the FHA mortgage insurance premiums effective March 20, 2023:

Unless you put down 10% or more, on an FHA loan the mortgage insurance premium is paid for the life of the loan. The cost of the mortgage insurance does decrease annually. If you do put down 10% or more, the mortgage insurance premium drops off after 11 years.

Despite a possible lower interest rate, for applicants with higher credit scores and higher down payments, the cumulative cost of the rate plus mortgage insurance will perhaps make FHA financing more expensive than conventional financing. Whereas you may find better terms with FHA is with lower credit scores & down payments.

FHA also has an upfront mortgage insurance premium of 1.75% which is financed into the loan amount. However if you were to streamline refinance your FHA loan into another FHA loan, within 3 years, you could get a partial refund of this premium back.

It’s important to note that the loan limits on FHA loans increase if you purchase a multi-unit property, and the minimum down payment is still 3.5%. These loan limits are effective for loan limits in 2023:

- 1 Unit: $1,249,125

- 2 Unit: $1,599,375

- 3 Unit: $1,933,200

- 4 Unit: $2,402,625

For condominiums FHA still offer whole building approvals. Since 2019 FHA also offers single unit approvals.

Pre-Qualify Now: https://ajaffe.firsthome.com/startapp

ajaffe@firsthome.com 240 – 479 – 7658