Blog

Medpal

Full time employees of Montgomery County and buying in Montgomery County may be eligible for Medpal, which provides a $50,000 forgivable down payment/closing cost assistance loan. This program is a part of the Maryland Mortgage Program but is an enhancement of the product, but only for county employees of...

Read MoreHome Ready and Home Possible

There are two really great loan programs offered by Fannie Mae (Home Ready) and Freddie Mac (Home Possible) that combine low down payment loans with superior mortgage terms. These products even have better terms in many cases than standard conventional financing at a variety of down payment amounts. Program Highlights: 3% Down minimum...

Read More

Federal Home Loan Bank

FHLB funds are currently exhausted until replenished! The Federal Home Loan Bank (FHLB) program provides a $15,000-$20,000 grant or forgivable loan to be used towards down payment and closing costs. There are three programs: The Workforce Housing Grant offers a $15,000 grant, to home buyers with incomes from...

Read MoreDown Payment Assistance Programs

There are down payment assistance and low down payment programs available both nationally and locally. I have written below the descriptions of each program to aid in understanding what is available. During your initial conversation, we will review your financial situation to see what is the best fit for you....

Read More

Bridge loan for a home purchase

We offer temporary financing, primarily meant to help finance your next home while you're still working to sell your current home. If you qualify we can place a bridge loan on either the home you're buying or the home you're selling, or both. We can simultaneously put together a refinance...

Read More

Homestead Deductions in DC and MD

If you buy your home in DC or in Maryland, and will live in the property, you will want to apply for the homestead deduction. The homestead deduction will limit how much your property taxes can increase annually and potentially reduce your tax bill. In DC, with the homestead deduction...

Read More

Insurance & Condo/Co-Op Changes

Fannie Mae and Freddie Mac announced the following changes that both ease and tighten insurance, condominiums, and co-ops lending guidelines. Here's what is easier, and this is effective now on conventional conforming financing: 2-10 unit condominium associations - in most cases we'll no longer need a condominium questionnaire nor need...

Read MoreAppraisal Waiver

Many buyers and agents ask if it's possible to purchase without an appraisal. Or, if they can waive an appraisal contingency in their contract without increasing their risk. The appraisal waiver / value acceptance can help with that - and here's how it works. Fannie Mae and Freddie Mac...

Read More

Family Lending

Mortgage guidelines have specific rules on allowable sources of funds for down payment and closing costs. In most instances gifts from family are allowed. Gifts are money that will never be repaid. Sometimes clients ask about getting loans from family for their purchase. This blog post overviews the rules for...

Read More

Gifts

I am not a tax advisor. But many clients have questions about how gifts both affect their mortgage application and their taxes. I am happy to explain: Gift amounts There is no limit to the amount of the gift. You may receive multiple gifts from multiple sources. 2. Gift sources...

Read More

Multi-Unit 5% Down

With a conventional loan we are now able to finance primary residence multi-unit properties of 2-4 units with 5% down without income limits/caps! To put down 5-24.99%, a buyer will need to occupy one of the units for minimally one year after purchasing. Learn more Https://alexjaffe.com/occupancy If a buyer wishes...

Read MoreUnderstanding Closing Costs

There are five primary categories of closing costs: Lender fees Title Attorney costs, including title insurance Transfer taxes to local government Real Estate Agent Commission/Fee Upfront deposits for escrows and prepaids In addition to the main categories, there are going to be miscellaneous costs which vary by transaction. For instance...

Read More

2026 Limits

Each year the Federal Housing Finance Agency (FHFA) announces changes to loan limits based on changes to average home prices. For 2025, loan limits for conforming and FHA loans are: Conforming or FHA: $832,750 Conforming Jumbo or FHA jumbo: $1,249,125 These numbers are increases from the 2025 numbers of $806k...

Read MoreServicing

Watch the video to learn more about mortgage servicing. Pre-Qualify Now: https://ajaffe.firsthome.com/startapp ajaffe@firsthome.com 240 – 479 – 7658

Read More

2025 Limits

Each year the Federal Housing Finance Agency (FHFA) announces changes to loan limits based on changes to average home prices. For 2025, loan limits for conforming and FHA loans are: Conforming or FHA: $806,500 Conforming Jumbo or FHA jumbo: $1,209,750 These numbers are increases from the 2024 numbers of $766k...

Read MoreDC Tax abatement

DC Tax abatement is an incredible program, which allows for: 1. The buyer does not pay for the recordation tax, which is .725%-1.45% of the sales price. Also, instead of the seller paying the transfer tax (1.1%-1.45%), that transfer tax is credited to the buyer. The net change is a...

Read More

Transfer Tax

First time buyer potential tax savings on closing costs: DC: .375% to .725 of purchase price MD: .25% of purchase price. In Maryland, home buyers who've never owned real estate in the state and are buying a primary residence are exempt from the state transfer tax, which saves .25%...

Read MoreSabotage

DON’T MOVE YOUR CASH/SAVINGS AROUND: We have to verify all funds for closing, including the source of those funds. Moving assets around can create a paper trail nightmare. The best advice is to leave everything where it is, even if the purpose of the move is to pool your funds...

Read MoreCo-signing

A co-signer is a mortgage loan applicant who co-applies with a home buyer to help the buyer qualify for their mortgage. This co-applicant is typically a family member who does not plan to occupy the property the home buyer is purchasing, and is therefore labeled a non-occupant co-borrower (or co-signer)....

Read MoreBuydown

An interest rate buydown will decrease the interest rate for the first 1-2 years. There exists in the mortgage industry both a 1 year buydown and also a 2-1 buydown. For example in a 1 year buydown, let's say the starting interest rate is 6%. For the first year, thanks...

Read MoreBuydowns

An interest rate buydown will decrease the interest rate for the first 1-2 years. There exists in the mortgage industry both a 1 year buydown and also a 2-1 buydown. For example in a 1 year buydown, let's say the starting interest rate is 6%. For the first year, thanks...

Read MoreHome Insurance

Home insurance on your new home is required to approve financing for your home. Home insurance is also often referred to as homeowner’s insurance or hazard insurance, and these terms are interchangeable. You’ll need to choose an insurance provider and agree to the coverage, deductibles, and cost for them...

Read MoreFHA100

FHA 100 is a new loan program featuring a down payment assistance loan of 3.5% or 5% of the purchase price. This down payment assistance loan is used to cover the minimum 3.5% down payment on an FHA loan. This loan product is available throughout DC, MD, VA and NC. ...

Read MoreHow do we determine how much you qualify for?

You may already have a payment range you've determined that would work for you. But when people think about getting pre-approved for a maximum loan amount, we have our own system for determining what we think would work for you. When asking about a maximum amount you can borrow,...

Read MoreCRA

We offer community reinvestment act (CRA) loan programs in DC, Maryland, Virginia which can offer improved loan terms to eligible buyers. An eligible home buyer could make just a 3%+ down payment on a conventional 30 year fixed loan and potentially not have mortgage insurance. These programs are for both...

Read MoreMcHaf

Montgomery County HOC opened 8/1/25 a fund of $2 Million to provide down payment assistance for eligible home purchasers in Montgomery County. The amount of assistance is up to $25,000 to be utilized for down payment or closing costs. To learn more about eligibility for the HOC program including income...

Read MoreCash to close

Cash to close refers to a combination of the down payment plus closing costs. The combination of the two makes up the cash to close, and the earnest money deposit is applied to the cash to close.

Read MoreFirst Home Advantage

Today we introduced the First Home Advantage loan product, which improves pricing of loans for eligible buyers, mostly for but not just limited to first time buyers. Fannie Mae and Freddie Mac, entities of the federal government, removed loan level pricing adjustments (LLPAs) on all Home Ready loans and also...

Read More

Home equity lines of credit

We offer home equity loans but not home equity lines of credit. A home equity line of credit (HELOC) is generally a 2nd mortgage loan you take out in addition to the loan that you currently have. Most homeowners take out a HELOC to finance home renovations. Or, you could...

Read MoreHome Equity Loan

A home equity loan is a secondary mortgage behind your existing loan! It allows you to cash out equity for a variety of purposes including financing renovations or consolidating higher interest rate debt. This loan is available on a primary or secondary residence. Your existing mortgage plus the new home...

Read MoreCommunity

This program is eligible for loans closing up until 6/20/25 and thereafter it will be closed. Our Community grant is paired with a conventional 30-year fixed mortgage, and is a $3,000-$5,000 grant depending on eligibility and income. It's available in MD, DC and VA. This grant may be used...

Read MoreTax Advantages

I am not a tax advisor - but I often get questions about the tax advantages of home ownership. The below deductions assume you choose to itemize your deductions instead of taking the standard deduction. Here are the benefits: Deduct interest: When filing your income taxes, you may deduct the...

Read More

Chenoa

The Alex Jaffe Mortgage Team now offers financing with no down payment from the buyer up to sales prices of $1,253,626*...and there is no income limit for the program! *Max sales price varies by county and $1,253,626 is applicable to DC and the counties that surround it, plus Frederick &...

Read MoreCo-ops

We’re able to help you finance your co-op in DC, MD or VA! Co-ops are a great option for home ownership in the DC metropolitan area that is very similar to buying a condo. Down payments can be as low as 3%-5%. There's a maximum loan amount of $1,209,750. The...

Read MoreEarnest Money Deposit

When making an offer, you will present to the seller an earnest money deposit (EMD). This deposit will ultimately go towards your cash to close, which is made up of your down payment and closing costs. We will be documenting as part of your loan application the EMD clearing your...

Read MoreLimited Review

Typically, Fannie Mae and Freddie Mac require a full review of a condominium association as part of our underwriting requirements when financing within a condominium. However, in some cases they can allow a limited review on a conventional loan for a condominium. A limited review will mean that we need request...

Read MoreBuy

My role as your loan officer is to help guide you in deciding how to best finance your home purchase. There are several loan programs to choose from, and the best choice for you is based on analysis of your income, debts, assets, credit, and your goals and long term plans....

Read MoreWhat can I use for a down payment?

The down payment is the difference between your loan amount and sales price. Closing costs are additional. The down payment and closing costs make up your cash to close. Down payment funds can come from a variety of sources, like: You can use liquid assets like a checking, money market...

Read MoreBuying versus renting

While there are many clear advantages of purchasing real estate, rather than renting, you should also consider the advantages and disadvatages of both before you make the important choice between the two. Why buy? To build equity - Each month that you make a mortgage payment, you'll build equity through...

Read MoreInvestor+

Our new investor+ loan product expands access to financing for investors. The key criteria and benefits are: Available for both individuals and LLCs! Up to $1.5 Million loan amounts 20%+ down for 1-unit properties, or 25%+ down for 2-4 unit properties Starting at 660+ credit scores This program...

Read MoreInvestment Property Loans

An investment property is a purchase for which the planned use of the property is usually for rental income. We are happy to lend on residential investment properties. On account of the greater risk associated with investment loans, these loans come with higher rates, higher down payment requirements, and slightly...

Read MoreWhat on my mortgage payment can change?

Your property taxes will adjust whenever your jurisdiction changes the assessment of your home. They may also change if tax credits are added or removed, for instance credits for occupying the property as your principal residence. Counties or cities will re-evaluate their tax rates, also, on an annual basis. Learn...

Read MoreRefinance

It's always a pleasure to help you understand the benefit, cost, and process of refinancing. Here is the key information that’ll help me provide guidance to you, and you can email me this info E-mail me. If you don't have all the answers to the below, that's OK!: Your property...

Read MoreRecast

A recast differs from a refinance. The purpose of a recast is to lower your monthly payment without having to take out a new loan. With a recast, you will pay down your principal balance and request the lender recalculate the lower mortgage payment based on the lower balance. In...

Read More

Reserve studies

In October 2022, Maryland joined Virginia in requiring that homeowners associations, condominiums, and cooperatives complete a reserve study every 5 years. DC does not have a reserve study requirement, currently. A reserve study is both a financial analysis of an association's balance sheet and budget, as well as an examination...

Read More

Property Taxes

The county, city, or state you choose to purchase in charges property taxes which are based on the assessed value of your home. These property taxes are typically included in your monthly payment in that 1/12th of your tax bill is paid into your escrow account. What is escrow? You...

Read MoreVA Loans

The VA loan is often the best possible loan because it offers lower costs than conventional financing. And regardless of down payment, there is no monthly mortgage insurance. There are no lender fees on VA loans and realtors are disallowed from charging fees as well. Unless you are exempt, the...

Read MorePoints

Points, origination points, and discount points are synonymous. Points are an upfront closing cost and are a charge based on your loan amount. One point refers to a charge of one percent of the loan amount. On a $400,000 loan amount one point is $4,000. Rates and points are connected...

Read MoreBridge Loans

It can be difficult to time the sale and the purchase of your next home perfectly. While it's ideal to sell and buy on the same day, sometimes you won't be able to sell your property before closing on your new home. If you have significant equity in your...

Read MorePrepayment

Prepaying will cut down on life of loan interest and pay off your loan more quickly. That's because interest is charged each month based on your outstanding balance. And so by paying your balance down early, you're making subsequent monthly payments allocate more to principal and less to interest. Prepaying...

Read MoreEscrow Analysis

Expect an escrow analysis once per year, mailed to you. Please be sure to read it to understand how your mortgage payment is changing. The escrow analysis looks back at property tax and insurance costs incurred over the last year. It’ll recalculate what should be your monthly payment to your...

Read More

Bank Statement Underwriting

Our bank statement program allows us to use 12 or 24 months of bank statements in lieu of tax returns to calculate income. This can be a helpful alternative for self-employed purchasers! This is a conventional 30-year fixed loan and is available starting with a 20%+ down payment. Two years...

Read More1st Time Advantage

Maryland Mortgage Program has numerous loan programs, and 1st Time Advantage is the most common Maryland Mortgage Program product we offer, because it comes with a down payment assistance loan of up to 5% of the loan amount. This program is for first time buyers in Maryland and is available...

Read MoreOne

First Home's One program offers up to a $5,500 grant, which is paired with a mortgage from First Home Mortgage. Pre-Qualify Now: https://ajaffe.firsthome.com/startapp One is available to buyers purchasing their home, both repeat and first time buyers. The grant is up to $5,500 or 2% of the purchase price whichever is...

Read More

2024 Limits

Each year the Federal Housing Finance Agency (FHFA) announces changes to loan limits based on changes to average home prices. For 2024, loan limits effective and available today are Conforming: $766,550 Conforming Jumbo: $1,149,825 See announcement here: https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Conforming-Loan-Limit-Values-for-2024.aspx These numbers are increases from the 2023 numbers of $726k & $1,089k. A...

Read More

Improving HPAP

Today I was given an opportunity to meet with DC Government and share insight on HPAP. DC homeownership (and housing) is unaffordable to many, and HPAP can fix that for some. And the tens of thousands of homeowners since 1980 who've been through the program successfully are a testament to...

Read More

FHOP

The Family Homeownership Program (FHOP) offers 100% financing without mortgage insurance for eligible buyers (no down payment required). Eligibility for the program is based on either a) meeting household income caps or b) buying in an area where there is no household income cap. Although being a first time home...

Read More

Solicitations

Both your home purchase as well as the mortgage on your property are recorded in public record after you purchase. Therefore, after you purchase you're highly likely to receive some solicitations by mail. It's also common for these solicitations to show the name of your lender on the envelope or...

Read MoreDream

Dream is available to home buyers who meet the underwriting requirements of either Home Ready or Home Possible. The $3,000 is a grant from First Home Mortgage. The mortgage the grant is paired with must also be obtained, and the mortgage and grant together are the Dream program. To qualify...

Read More

OptOut

There are 3 credit bureaus: Equifax, Transunion and Experian. The credit bureaus are businesses, and one line of business they are in, is in selling leads to creditors. For instance, competing mortgage lenders can pay the bureaus to be informed when someone pre-qualifies for a mortgage loan. The home buyer...

Read More

Greenbelt Home Advantage

UPDATE: This program has exhausted funds and it's unknown whether it'll be funded again. Greenbelt Home Advantage is an enhancement of the Maryland Mortgage Program (MMP), for eligible purchasers. Learn more about MMP here: https://alexjaffe.com/md-down-payment-assistance This program offers a grant of $15,000 to home buyers purchasing within Greenbelt (zip...

Read MorePITI

The acronym PITI refers to principal, interest, tax and insurance. These are the components of the monthly mortgage payment you'll be making. If you purchase a property that is a part of a homeowners association, co-op, or condo, we might use the acronym PITIA where "A" refers to the association...

Read More

Rental income

We're able to consider rental income in qualifying on a loan application, subject to these underwriting rules that are within written lending guidelines. There are three different categories of rental income: Rental income from investment properties currently owned. Projected rental income from the property being purchased Rental income that'll be...

Read MoreHeroes

We're proud to launch First Home Heroes, to recognize the heroes in our community. First Home Mortgage is now crediting back / covering lender fees for first responders, teachers, and medical professionals. This leads to a savings in closing costs of up to $1,935 and it's our way of...

Read More

Housing Solstice

I'm Alex Jaffe, I work for First Home Mortgage, and we finance homes here in DC, MD and VA. I’m going to explain how financial conditions are impacting the housing market, why in 2022 so many Americans lost interest in purchasing a home which was a reversal from last year,...

Read More

2023 Loan Limits

Each year the Federal Housing Finance Agency (FHFA) announces changes to loan limits based on changes to average home prices. For 2023, loan limits effective and available today are Conforming: $726,200 Conforming Jumbo: $1,089,300 These numbers are increases from the 2022 numbers of $647k & $970k. A conforming loan allows...

Read MoreCP

We offer construction-to-permanent (CP) financing which finances construction/building of a new property that'll be your home (primary residence). This loan can be utilized and be combined with financing and purchasing the land, or on land you already own. CP financing is similar to renovation financing, but CP financing does not...

Read More

VA and FHA Approved Condos

Some condo projects have already been reviewed and approved by VA or FHA. Here’s where and how to search if your condo has already been approved for each type of financing. For VA loans, the VA (Veterans Affairs) must review and approve the condo project themselves. VA condo...

Read More

FHA Single Unit Approval

In October 2019, FHA (Federal Housing Administration) introduced the Single Unit Approval (SUA). This allows us to approve individual condominium units within a condominium that doesn't have an existing approval for the condo association as a whole. The SUA provides a much quicker review process to approve an individual condo...

Read More

Crescendo

Imagine the housing market of early 2020-2022 as an orchestra. The musicians are comprised of loan officers like myself, realtors, and the buyers and sellers who’ve been trading real estate over the past two years. Imagine the buyers and sellers as the drums - setting the pace. I'm playing the...

Read MoreFirst Payment

Mortgage payments are due on the 1st of the month. However they are not considered late unless the payment is received after the 15th of the month. And so your payment is "on time" if it's received at any point up to the 15th. The "June 1st" payment is not...

Read More

Estimating DC Property Taxes

Here is a tutorial to how I estimate property taxes. DC's property tax rate for Class 1 residential property is .85%/year of the assessed value. So if a property is assessed at $100,000, the annual taxes would therefore be $850 a year. However DC homeowners might have reductions to their...

Read More

Towns on Grove

As of 5/3/21, Towns on Grove is now sold out. Hi! Thank you for your interest in pre-qualifying to purchase workforce housing for the Towns on Grove. It's a pleasure to be of assistance. This website serves as instructions for how to begin. All adults in the household should apply...

Read More

2021 Loan limits

Each year, the Federal Housing Finance Agency publishes loan limits. These loan limits impact financing on almost every loan program. 2021 loan limits are out! The 2021 conforming maximum limit is now $548,250 (minimum 3% down) The 2021 jumbo conforming maximum limit is now $822,375 (minimum 5% down) By...

Read More

Stability

Almost 200,000 Americans, and over 900,000 humans have passed away this year from Covid-19. I’ve been through excruciatingly difficult conversations with friends who’ve lost parents and siblings. Two friends have had to close their businesses permanently. My brother was supposed to get married on Saturday; but he and his fiancé...

Read More

Volatility

In the first week of March, mortgage rates hit historic lows. For a brief moment in time, 30 year rates reached the low to mid 3s and 15 year rates hit the high 2s to low 3s. Our company, First Home Mortgage which is the largest lender in MD and 4th largest lender...

Read More

Springboard

April 2020 update: this program is currently suspended. See other programs which are currently available at https://alexjaffe.com/dpa We just released the Springboard down payment assistance program, which is available for home buyers in Maryland & Virginia! This is a conventional loan program without mortgage insurance which comes with a repayable down...

Read MoreBorrowSmart

BorrowSmart is a grant program offering $1,250 in grant funds, available if you're under 80% of the area median income AND putting down less than 20%. The program cannot generally be paired with other assistance programs. The assistance is paired with a 3%+ down conventional Home Possible loan and is...

Read More

Amazon HQ2 comes to Crystal City DC area…now what?

Crystal City, VA is home to Amazon's 2nd headquarters (HQ2). If you're considering a job opportunity to work here, acquiring a mortgage to finance a home nearby may be simpler than you think. Learn more about mortgage options and ways to commute! Closing on a home prior to starting...

Read More

Mortgage insurance is less now

This week, all six mortgage insurance companies that exist in the US either released or announced reductions to their mortgage insurance premiums. (Need to learn more about MI? Click here). I am reflecting back to when I started in this business in 2007. Between 2007 and 2015, mortgage insurance costs...

Read MoreRetirement

It is generally possible to utilize funds from a retirement account towards the down payment or closing costs for your home purchase. The rules for tapping into retirement accounts will vary, depending on the type of account(s) you have. I will list the typical rules for each account type, in...

Read More

Credit scores

Most home purchasers know that there are three credit bureaus: Experian, Equifax, and Transunion. These bureaus are repositories of information from all participating creditors. Before credit scores existed, credit bureaus collected and provided information about creditworthiness to lenders. The first credit score was created in 1989 by the Fair Isaac...

Read More

Down Payment Assistance

There are down payment assistance and low down payment programs available both nationally and locally. I have written below the descriptions of each program to aid in understanding what is available. During your initial conversation, we will review your financial situation to see what is the best fit for you....

Read MoreEmployment history

Whenever you apply for a loan, you'll be required to provide a two year history of either employment or time in school. If your income is salaried, we'll calculate and qualify your income based on your salary. If your income is variable and is hourly, bonus, commission, or via tips, we'll...

Read More

Loan Limits Increase in 2018

Beginning with closings in 2018, the new conforming loan limit is $679,650. This'll be the maximum loan for a 5% down one-loan-scenario, which will be a purchase price of $715,421. However, 5% down will be available up to purchase prices of $978,578 with financing with two loans. 3% down will...

Read More

Loans

Conventional Loans - Best paired with higher credit and/or higher down payment...providing the best terms for most applicants FHA Loans - Best paired with lower credit and/or lower down payments...providing superior loan terms in the above instances Jumbo Loans - For loan amounts over $1,209,750, jumbo loans require slightly higher down...

Read MoreOccupancy

There are three types of ways you can utilize a property you are financing. They are a primary residence, second home, or investment property. A primary residence is a home in which you live in as your principal residence, and typically occupy at least a majority of the year. In...

Read More

Inquiries

Many people ask what type of inquiry is associated with a mortgage pre-qualification. Anytime you apply for credit it's a hard inquiry. When you apply for non-credit things, like utilities, employment, insurance, that is more likely a soft inquiry, but depending on the circumstances it could be a hard inquiry...

Read More

Termite Inspections

Termite inspections are typically not required. But, let's learn about when we do need to review the report. The VA loan is the only product which requires a termite report to be completed and reviewed by us. The only exception is if the buyer is using VA financing to purchase a...

Read More

FHA Condo Approval

We process FHA submissions in house and submit them to the Department of Housing and Urban Development (HUD). Their review will likely take 2 weeks to 30 days. FHA condominium approvals are valid for the entire project for two years. Prior to December 2009, once approved a condo was always...

Read MoreVA Condo Approval

The Department of Veterans Affairs (VA) requires they review and approve a condominium prior to financing a loan in each condo project. In our experience the VA review can take anywhere from 2-4 weeks to complete, but once approved, the condo approval does not expire and can be used on...

Read MoreCondo

If you want to learn about condos...you've come to the right page. Click on the links which interest you to learn about condominiums, condo fees, and what we review when analyzing whether a condominium association is suitable for financing. Condominiums (General) Primary Criteria for Condo Approvals Limited Reviews for Condos (Easier...

Read More

CPM

Learn about conventional condominium and co-op underwriting with Condo Project Manager (CPM) and how we can support buyers and realtors pursuing condos and co-ops because of it. When we finance a condo or co-op, we typically have to review the insurance, finances, and any inspection or reserve study done within...

Read More

PERS

Fannie Mae has a Project Eligibility Review Service (PERS) approval option which is useful in the following three scenarios: Non-gut condominium conversions New projects with units under 400 square feet (micro units) Condo project consisting of manufactured homes A PERS approval is a submission to Fannie Mae, and often avoided...

Read More

New Construction Condos

In addition to meeting all of the existing condominium requirements, there are a few additional steps required when a condominium is newly built or newly converted. A condominium is defined as new if it meets any one of these classifications: The developer is still in control of the condo association Construction...

Read More

2-4 Unit Condos

This site explains the standard requirements for condo approval. But, for a condo with 2-4 units, we are not required to review the project other than making sure the condominium: a. Has adequate insurance and meets requirements as laid out here. b. Is not operated like a hotel or motel...is...

Read More

Montgomery County $25k Assistance

The MMP program has a new option in Montgomery County! Purchasers can now apply for Montgomery Homeownership Program VIII which provides up to $25,000 in down payment and closing cost assistance. The amount of assistance is determined by your household income, and is set at 40% of your total...

Read More

Condo Insurance

For conventional loans, both Fannie Mae and Freddie Mac require condos to have specific coverages included in their master insurance policy to approve the condo project for financing. Both Full Review and Limited Review methods require the following coverages and endorsement requirements: Building coverage must document Replacement Cost Coverage, Extended Replacement Cost, or Guaranteed...

Read MoreCondo Approval

When using conventional financing to purchase a condo, we’ll need to review the condo and verify it meets Fannie Mae and Freddie Mac’s guidelines. Depending on the down payment, residency, and type of condo, the condo review may be a 2-4 Unit Review(https://alexjaffe.com/2-4-units/), a Limited Review, or a Full Review....

Read More

Condos

If a buyer is financing a condominium or a property in a homeowner's association, we are required to determine if the association meets the standards of Fannie Mae or Freddie Mac. The primary difference between the two types of ownership are that in a condominium, together the members of the...

Read More

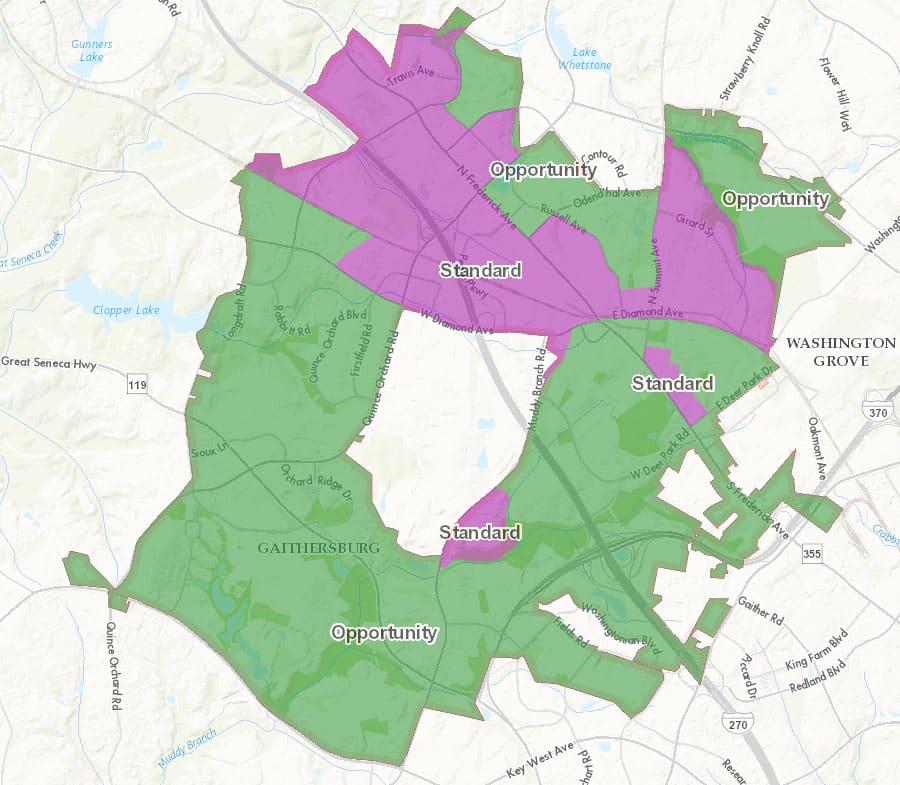

Gaithersburg Homebuyer Assistance Loan Program

The city of Gaithersburg provides down payment and closing cost assistance for purchasers in the amount of $12,000 (blue areas) or $25,000 (yellow areas). You will repay the assistance without any interest due. You may finance this loan alongside an FHA or Conventional or VA loan program. The minimum credit...

Read More

Seller Credits

In addition to the down payment, a buyer will pay closing costs in connection with their purchase. If the combined amount of cash required is more than a buyer is comfortable with, then they may attempt to negotiate a seller credit for some or all of the closing costs. For example:...

Read More

Condo Fees

If you purchase in a cooperative, condominium or homeowner's association, you will pay a fee to the association. This fee is determined by the square footage your home represents in the overall square footage of the association - you will pay a percentage of the costs. The members of the association...

Read MoreStudent Loans

It's important to understand how your student loans affect your ability to qualify for your mortgage. For most people, the monthly payment of your student loans is more important than the balance. How it affects your qualifying ability depends on which loan program you select. Make sure to check out...

Read More

How do rate changes affect your payment?

When interest rates rise, you may be concerned about how that affects your affordability of your monthly payment. Let's break down how a rate shift affects your monthly payment on a 30 year fixed loan. For every $100,000 you borrow, a 1% change in the interest rate will shift the...

Read More

Maryland Grant Assist

Effective 5/18/22 this program is suspended until the state re opens the program. The Maryland Mortgage Program released a new grant program in 2017. Buyers can receive down payment and/or closing cost assistance of 4% of the loan amount. This grant comes from the state. It does not need to...

Read More

MCC

As of 9/27/22 the MCC in DC is suspended due to funds being exhausted. The below references regarding the program being available in DC are hopefully available again once the program is funded. Maryland no longer offers MCCs (as of June 2020) As of 4/10/23 Virginia is also suspending MCCs....

Read MoreARMs

Adjustable Rate Mortgages (ARMs) offer lower start rates on mortgages with the risk that the rate will adjust in the future. The most common ARM is the 7 year ARM, wherein the rate is set for 7 years but then adjusts annually after that. But there are also 3, 5,...

Read More

DC Lowers Transfer Taxes for First Timers

DC's city council just voted in a reduction in transfer taxes to .725% of the purchase price. This is a first time buyer benefit for eligible purchasers whose income is less than 180% of the area median income. That income cap is going to be approximately $190k a year. This...

Read More DC Open Doors Top Producer

The DC Housing Finance Agency just celebrated its third anniversary and the close of the third fiscal year of the DC Open Doors program. I have been fortunate to be recognized as the top producer of the program every year, as well as being the loan officer who closed the...

Read More FHA Condo changes

If you're seeking to buy a condo and looking to put a minimal amount down, then you may be looking to get an FHA loan. FHA has been more strict on whether they'll lend in a condominium project in the last several years. But yesterday they eased up on one...

Read More 5% Down to $625,500 and more good news

Thanks to Fannie Mae changes Saturday, we no longer require 10% down on loan amounts of $417,001 to $625,500; now primary residence purchasers only need to put down 5%! Also, all of the down payment can come from family gifts, even when the buyer is purchasing with a co-signer. Conforming...

Read More Clear to close in 14-21 days

The new TRID requirements have lead to a big change in the industry with regard to how we approve and close loans. However, TRID has also been an opportunity to deliver even better customer service, which was the intent of the new law. Our adjustment has been smooth. We have...

Read MoreMortgage Insurance Options

Mortgage Insurance covers the risk a lender takes on, in a case a borrower defaults on their loan. On a conventional loan, a home buyer pays private mortgage insurance (PMI). There are six mortgage insurance companies nationally and they set pricing for MI based upon risk, and the most important...

Read More Top Producer for DC Open Doors – Alex Jaffe

I am thrilled to share that for the second year in a row, I provided the most DC Open Doors loans to home buyers in Washington DC. More info on DC Open Doors is found here. 0% down financing for Washington DC buyers thanks to a 3-3.5% down payment assistance...

Read More Condos with high delinquencies

I am pleased to share that we have expanded our guidelines on condominium approvals for conforming loans. Until now, buyers using Fannie Mae financing were required to put down 20% if they were attempting to purchase a condo with high delinquencies. Now, using Freddie Mac financing, we can perform a limited...

Read More FHA Reduces Mortgage Insurance Premium!

Great news! HUD just announced that the mortgage insurance rates on FHA loans will be reduced with new registrations of 1/26/15 or later. The new mortgage insurance rate will be .85% for loans with less than five percent down, or .8% for loans with five percent down or more. On a $400,000 loan this...

Read More Conventional Renovation – Homestyle

I'm pleased to share that we now offer conventional renovation loans, called the homestyle program. The use of this program is for a purchaser who would like to finance the purchase of a property and also receive financing for renovations and repairs. Previously, there was only the FHA 203k loan...

Read More DC Open Doors announces .25% rate reduction

DC Open Doors http://www.dchfa.org is now offering a .25% rate reduction on its loans with down payment assistance. This is terrific for some buyers who are interested in the program but some restrictions apply. This loan program is called the Mortgage Revenue Bond program, because it is funded by the...

Read More Rent versus Own Data in Washington, DC

Zillow compiled an incredible amount of data from every zip code in the United States to calculate how long you should plan to stay in your home so that owning makes more financial sense than renting. Here is their data for Washington, DC. Zillow's calculations are typically based on 20%...

Read MoreDC Open Doors

Zero down payment purchase financing in Washington DC that most people qualify for. And it’s easy! New income cap for 2017: $132,360 (based on borrower income, not household income). Maximum loan amount for 2018 is $679,650 for 3% down financing or $453,100 for 0% down financing. Watch the video for...

Read More New head of FHFA, Mel Watts, delays/reconsiders increasing rates

Per a news release today from the Federal Housing Finance Administration, the FHFA will delay the guarantee fee increase that was scheduled to take effect this Winter. This would have resulted in an across-the-board .25% increase for every conforming loan. New director, Mel Watts, wants to reconsider the effect...

Read More Self-Employed Borrowers

Listing agents may be wary of accepting contracts from self-employed borrowers for a few reasons, so I thought I'd share these challenges and how we overcome them. Problem: Many loan officers simply don't know how to calculate self-employed income The number one reason why self-employed borrowers get a bad reputation...

Read More No down payment required in Washington DC

Thanks to the new loan program that we offer through the DC housing finance agency (DCHFA), home buyers in Washington DC do not need their own funds for a down payment! The program will provide the needed funds for the down payment, and provided you live in the property for...

Read More We have a Yelp page

Please review me on Yelp! I would love it if you'd share your experience with others. http://www.yelp.com/biz/first-home-mortgage-chevy-chase-md-chevy-chase

Read More Washington, DC 2013 First Time Buyer benefits

In December, 2012, DC updated its first time buyer benefits. I'm referring specifically to the DC Tax abatement, which allows for: 1. The buyer does not pay for the recordation tax, which is 1.1% of the sales price. Also, instead of the seller paying the transfer tax (also 1.1%),...

Read More Maryland First Time Buyer Benefits

In the state of Maryland, as a first time property owner, you are eligible to avoid the state transfer tax which is .25% of the sales price. Other than that, there are down payment assistance programs both with the state and with Montgomery County. For a one to two person...

Read More DC First Time Buyer Benefits

You may be eligible for a first time buyer credit of $5000. Here is the IRS tax form: http://www.irs.gov/pub/irs-pdf/f8859.pdf DC's page on the subject: http://otr.cfo.dc.gov/otr/cwp/view,a,1330,q,594156.asp The issue is that they haven't yet extended the credit for 2012 yet. See the IRS form for income restrictions, if you are buying as...

Read More Launched my videos!

Thanks to Trent Watts at Watts Media Productions, I now have fifteen different videos uploaded answering frequently asked questions about mortgages. I'm excited to share this new form of information with you all.

Read More FHA Mortgage Insurance

Per President Obama's press conference today 3/6/12, it looks like he'll be cutting in half the mortgage insurance on FHA streamline refinances. We await additional information but this is great news thus far!

Read MoreWhat is APR?

Annual Percentage Rate, or APR, is the most commonly misunderstood term in borrowing. The use of APR was required as of the Truth In Lending Act, the purpose being to help prospective borrowers understand the cost difference between rate offers. APR, unlike the interest rate, offers a look at the true cost...

Read MoreWhat determines my rate?

1. What the market is doing. The market for interest rates moves on a minutely basis and most interest rates rise and fall with the sale of mortgage-backed securities. The market is open 8-5 on business days. Because rates constantly change, it's possible to lock interest rates after you have...

Read MoreWhy would I refinance?

First off, what is a refinance? A refinance (refi) is where you take out a new loan, with new terms, and use that money to pay off your old loan. You are “re-financing” your home. You would refinance for the following two reasons: To save money. This is a rate...

Read MoreWhat is mortgage insurance?

To protect against losses on low-down-payment loans, lenders require mortgage insurance for any loan-to-value higher than 80%. This is applicable for all conforming conventional Fannie/Freddie loans. In case of default, a mortgage insurer would pay a claim to the holder of the mortgage. Because of the cost of foreclosure, a mortgage...

Read MoreMortgage Insurance Cancelation

On a conventional one unit Primary or Secondary residence (loans originated after 1999): The Homeowners Protection Act of 1998 requires mortgage insurance to be canceled automatically when your loan balance is scheduled (based on the original amortization schedule) to reach a value of 78% of the purchase price. Canceling mortgage...

Read MoreWhat are the steps for applying for a loan?

1. Pre-qualification: A pre-qualification is the first step and answers the following questions: What is the best loan type for me? How much money will I need to put down? What kind of payments should I expect at the sales prices I am interested in? How much cash total will...

Read MoreHow do I calculate my ARM adjustment?

An adjustable rate mortgage, or ARM, typically has a start-rate that is set for a period of 3, 5, 7, or 10 years. After that initial period most ARMs adjust annually. How they adjust will depend upon the terms agreed to in your note, or shown on your adjustable rate...

Read MoreWhat is escrow?

Escrow has multiple meanings, but when we refer to escrowing mortgage payments, we refer to this: We the lender will be responsible for holding your property tax and insurance money and will make the payments of these bills for you. When you make your monthly mortgage payment, not only...

Read MoreHow do I improve my credit score?

The best way to improve your credit score will depend on your individual situation. But here are some great tips: 1. Whatever you do, the most important thing is to make sure you don't get any collections. Setup automatic payments for utilities if you can, and make sure your...

Read More Common Mistakes Made by Home Buyers

1. Assuming you qualify, or don't qualify, for a loan. There are many things we consider when determining whether to lend to a potential home buyer. What you read in the newspaper regarding requirements is not necessarily true. What one loan officer tells you is their policy, is not...

Read MoreHow do I appeal my property tax?

After you purchase your home, you're going to start receiving annual property tax bills. A copy of the bill will also be sent to your lender if you are escrowing your property taxes. Many people, when seeing their assessments rise, will want to appeal their taxes. Most jurisdictions will want...

Read MoreWhat documents do I need to provide?

1. Photo ID 2. A month's worth of paystubs if applicable 3. Two years of federal tax returns and W2s or 1099s 4. Two month's worth of bank statements or investment accounts. If you receive quarterly statements, the last quarterly statement is fine.

Read MoreWhat is a pre-approval and why do I need one?

You and the agent you are working with do not want to spend time looking in the wrong price range. Or, if you need credit repair, you and the agent wouldn't want to look at inventory now when you won't be ready to purchase for another few months. The...

Read MoreHow do I get pre-qualified?

The first step is to speak to your loan officer. You'll want to know the following: 1. Your gross income 2. Your available cash for a down payment 3. Your monthly debts 4. Potential locations and types of properties you are interested in By providing us with your income/assets/debts,...

Read MoreWhat credit score do I need to get a mortgage?

An FHA or VA loan will typically require a credit score in the 600s. A conventional loan will become possible at higher scores - the minimum will depend on other factors like down payment and debt-to-income ratio. The lowest possible score however is 620. We check credit scores with Experian,...

Read More How much down payment do I need in Washington DC?

A common misconception is that you'll need a 20% down payment to receive mortgage financing for a home purchase. You can actually get a loan with as low as 3.5% down, or 0% down if you are a VA eligible veteran. Specifically for first time buyers, there are actually...

Read More Conservator’s report – state on Fannie & Freddie

Full report here: http://www.fhfa.gov/webfiles/16591/ConservatorsRpt82610.pdf FHFA, linked above, wrote a report on the state of Fannie Mae & Freddie Mac. Here are some interesting pieces of it. All data is from Fannie Mae's stats: 1. This year's average credit score is 758 versus 716 in 2007. 2. 8% of loans...

Read More FHA’s new mortgage insurance

Want to put less than 5 or 10% down? You're likely going to get an FHA loan. Due to increased risk of defaults, HUD earlier this year increased its upfront mortgage insurance premium (MIP) from 1.75 to 2.25%. Now, starting in October, they are increasing the annual premium while decreasing...

Read More Rates

I just read this article that said out of the last 8 weeks, 7 of these weeks showed record lows for mortgage rates. Granted, these are small drops, but it just goes to show how far rates have fallen. I'm seeing 30 year fixed rates in the range of 4.25-4.75%. 15...

Read More MI Rates Fall for Well Qualified

Some of our MI providers have now instituted risk-based pricing models. Now your credit score, debt ratio, property type, and location are analyzed together to determine what your MI rate will be. After running a few sample tests, I've noticed that the most well qualified borrowers are getting nice...

Read More Flood Insurance

Interested in buying a property in a floodplain (special hazardous flood area) which requires flood insurance? Well, you haven't been able to since the National Flood Insurance Program expired May 31st. So the whole month of June halted all settlements which are in flood-risky areas. Locally, that means parts of...

Read More Required Documentation

Many buyers are curious about what documentation these days is required and why. The core documents are the ones that prove your income, your assets, and your identity: Last two paystubs/W2s and/or last two years of tax returns Last two months of bank statements and other asset accounts ID ...

Read More