USDA / Rural Housing loan

A USDA / Rural Housing loan is a zero down payment loan built for rural parts of the country.

A Rural Housing loan typically has better loan terms to FHA financing and would be an alternative to FHA. If you were considering FHA financing and want to borrow in a rural area, the Rural Housing loan may be right for you.

Like FHA, the Rural Housing loan has an upfront mortgage insurance premium which you must finance into the loan amount. But it’s 1% instead of 1.75%. Also the annual mortgage insurance cost is .35% compared to FHA’s .55%. So compared to FHA you will save annually .2%. On a $300,000 sales price this is about $600 in savings per year.

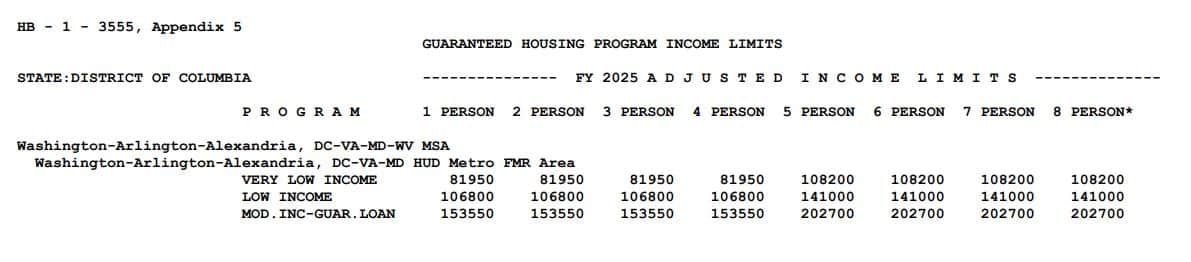

USDA has income caps based on household size (the maximum income allowed is 115% of area median income) and you can check out the income caps here: https://eligibility.sc.egov.usda.gov/eligibility/incomeEligibilityAction.do?pageAction=state

Interested in this type of loan, or another? Please pre-qualify here

After you go under contract to purchase a property, we underwrite your file, and then after completing it we send it to USDA for their review. And so USDA loans will take longer to process than other loan programs for this reason.

USDA will ordinarily allow you to spend 29% of your income on your housing payment and up to 41% of your income on all monthly debts. But if their automated underwriting software (GUS) approves a higher amount than that, then that is also acceptable, with restrictions.

USDA requires you occupy the property throughout the entirety of the loan, which is more strict than most other loan programs. To move out, you’d either sell or pay off the loan first. Learn more https://alexjaffe.com/occupancy

Please click here to check whether certain areas are eligible for USDA.